OVERVIEW

If you’re a multinational corporation with a healthy risk appetite, forget about investing in the BRICS[i] and start looking at frontier markets. Over the past few years, frontier markets have been receiving greater attention from international market participants seeking greater returns on investment and more markets to flog their products and services. These countries at the nascent stages of economic and political development constitute an attractive, if risky, opportunity for investors hungry for diversification and growth. These were markets historically viewed as “Third World” countries, too corrupt and unstable for sophisticated market participants to even consider. However, these developing economies tend to possess signs of great potential. Broadly speaking, these countries have a growing middle class, promising demographics, relatively low debt burdens, and stronger opportunities for economic growth, when compared to emerging markets.[ii]

Although the above characteristics form part of frontier markets’ profiles, these countries also exhibit significant risks.[iii] Many of these markets lack robust governance structures, strong democratic institutions or legal traditions. Located in geopolitical “hot zones,” instability and political violence are par for the course, these countries tend to lack the basic societal, political and physical infrastructure needed for lasting peace and prosperity and sustained progress. Further, some of these markets suffer from a dearth of property right protections and, crucially, the rule of law. Overall, frontier markets suffer from significant social, political and financial unpredictability.

Nevertheless, frontier markets have some of the strongest growth rates in the world;[iv] many of which are on the cusp of becoming the emerging markets of the future. Therefore, robust strategies for market entry can over time produce significant dividends.

WHAT ARE “FRONTIER MARKETS?”

According to Schroders PLC, a global investment manager, frontier markets “typically include a low/middle income country and a relatively under-developed capital market compared to their more developed Global Emerging Markets (GEMs) peers.”[v] The MSCI Frontier Market Index identifies the following 29 countries (as of May 31, 2018) as frontier markets: Argentina, Bahrain, Bangladesh, Burkina Faso, Benin, Croatia, Estonia, Guinea-Bissau, Ivory Coast, Jordan, Kenya, Kuwait, Lebanon, Lithuania, Kazakhstan, Mauritius, Mali, Morocco, Niger, Nigeria, Oman, Romania, Serbia, Senegal, Slovenia, Sri Lanka, Togo, Tunisia and Vietnam.[vi]

These markets have become increasingly attractive to global market participants because of their potential to provide access to some of the fastest growing economies in the world.[vii] These countries, however, have traditionally been wracked with political instability, tough business climates, a lack of robust civil and political institutions, and have offered a limited degree of access to foreign companies attempting to gain access to their markets; this has made investing in frontier markets a difficult and deeply risky proposition.[viii] But with risk comes great opportunity and as emerging markets wane, corporations are poised to invest to a greater degree in these frontier markets.[ix]

Corporations, as we all know, are growth and profit-seeking enterprises and will search the globe for maximal returns. This means seeking new and dynamic opportunities, lowering their costs, and opening up access to raw materials and various other resources.[x] What they are met with, particularly within the context of frontier markets, are risky and complex business environments. Therefore within the context of frontier markets, the question for market participants is—how can we, as multinationals, conceptualize and manage political risk to capitalize on the myriad opportunities that frontier markets can provide?[xi]

MANAGING POLITICAL RISK IN FRONTIER MARKETS

The Economist defines political risk as “the danger that the actions of governments might reduce the cash-flows that investors expect from their investments.”[xii] As such, understanding and managing political risk is central to investing and doing business in frontier markets. To that end, a simple political risk framework is essential for success.

Luckily, the management of political risk, whether in frontier markets, emerging markets or developed nations remains the same. The process relies on three steps which lead to; the avoidance, the acceptance, or the mitigation of risks. These steps are as follows; firstly, the identification of political risk—what are the challenges / opportunities we will be facing? Secondly, assessing that risk—how will these challenges impact the performance of the company in the frontier market? Finally, a mitigation strategy—what decisions can we make now, and throughout our investment tenure, to mitigate these risks?[xiii]

Identification of Political Risk

Serious market participants understand that their ability to assess and manage political risks is dependent on their ability to determine the kinds of risks they face.[xiv] These risks have two basic categories, firm-specific and country specific risks. Firm-specific risks are risks that impact the company on the project and corporate level such as, creeping expropriation, breach of contract, discriminatory regulations, sabotage, and boycotts. Whilst country specific risks have broader implications, such as, government corruption, civil wars, political violence, rioting, currency inconvertibility and nationalizations of industries.[xv]

Assessment of Political Risk

After identifying the precise risks that the company is likely to be exposed to in a frontier market, the firm can use tools to quantify the impact of those risks. For example, if a multinational firm is operating in the mining sector, a regulatory impact analysis can be used to determine the effects of proposed, existing and non-regulatory alternatives on their business practices.[xvi] Such an analysis will help the firm determine the strongest approach to counter or incorporate the business reality. It is an approach that will move the company toward understanding how it can best operate within its sector. Another tool at the company’s disposal is war gaming or decision role-playing.

War gaming allows multinationals to imagine the business environment in a controlled space and role play, examine and hone the strategies they begin to develop based on the risks they have determined to be key.[xvii] This technique evolved from its origins in the military domain. It has become an integral tool that multination firms can use, and rely on, to develop and implement core decisions, based on sound intelligence and truly assess the risks, the challenges, and opportunities that confront them in frontier markets.[xviii]

Mitigation of Political Risk.

This third step is also crucial; at this stage the risks have been identified and assessed, and the firm can decide whether to avoid the risk, insure against the risk, or develop a strategy to mitigate and monitor the risk. So what is needed now is for the company to implement a strategy to manage the political risk factors previously assessed.[xix] For example, a multinational operating in a country with a high corporate tax burden, may find it unattractive to stay given the costs. Whereas, a multinational firm, operating in a frontier market where government corruption abounds, may strive to overhaul its code of ethics and will prioritize its creative ethics training activities to guarantee that all rules are completely understood and thoroughly adhered to.[xx] Once a company has determined a political risk strategy, it is not enough to implement a one-time strategy to deal with the risk.

Political risk is an ongoing, ever-changing factor of business in frontier markets and across the globe. Therefore, part of dealing with risk is monitoring said risk. The integration of political risk into the enterprise risk function of any company wishing to operate in frontier markets where volatility and instability are more pronounced is an essential element of managing risk in those markets.[xxi]

MEASURING VOLATILITY USING THE J CURVE

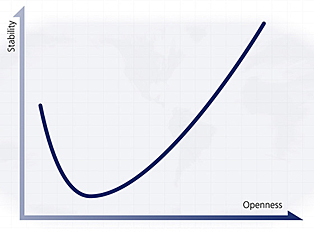

One framework that has been considered for measuring stability and political risks in frontier markets is the J Curve.[xxii] The J Curve was reformulated by Ian Bremmer, founder of political risk firm Eurasia Group, to help multinational companies, investors and consumers of international political data, gain greater insight into how states are affected by political and economic tumult. The framework does this by looking at the interplay between stability and openness in a society.[xxiii] Some have criticized the framework as either overly hopeful or too simplistic.[xxiv] However, the framework does allow market participants to begin their understanding of the interplay between stability and openness in a society.[xxv]

The above image[xxvi] is a visual representation of the J Curve; but what does it tell us and why is it useful? What the curve represents is a cross-section of countries with differing governmental systems; the curve displays what that means in terms of their level of stability or instability. Therefore, the stability of states is dependent on where they are located on the curve. States on the upper-lefthand side of the curve generally tend to be authoritarian; reliant on a central figure/leader, or a cabal. These regimes usually limit access to information and limit the dissent of their citizens. Whereas on the upper-righthand side of the curve, those states tend to be more open with established institutions, independent branches of government, and an informed citizenry that keeps their government in check.[xxvii] It also shows that there can be stability when a country is “closed” and when a country is “open.” The dip shows that when a country liberalizes or transitions towards greater openness, instability may be a byproduct which can be detrimental to the business environment.[xxviii]

This knowledge gives multinational firms the ability, based on their risk appetite, to establish a strategy to best mitigate the challenges they will face in a frontier marketplace. Frontier markets span the curve; they are diverse geographically and are at differing stages of economic maturity. They range from rich oil producers in the Gulf to poor underdeveloped states in Africa.[xxix] Therefore, the first question a company needs to ask, as they debate whether or not to access a frontier market, is; how will the country’s position on the curve affect the decision to access that market? And secondly, what risks will that expose the company to?

An example of the potential risks is found in Nigeria, Africa’s leading crude oil producer.[xxx] The country has begun reform to its oil and gas industry; these reforms are targeted at renegotiating production sharing agreements and allow the government to absorb a larger share of the revenues generated.[xxxi] Many of the global oil producing companies with a stake in the industry were unaware of this potential change and still remain uncertain about its scope.[xxxii] An analysis using the J Curve would have allowed these companies to identify the potential risk of creeping expropriation and thereafter formulate strategies to cope. Nigeria struggles with corruption, poor governance, and religious conflict but is also a democracy.[xxxiii]

This positions it within ‘the dip’ of the J Curve being neither fully open nor closed. One can therefore surmise that Nigeria may potentially have an unstable business environment. Information is the key to mitigating the risk; knowledge of Nigeria’s troubled political system and tumultuous oil and gas industry would have allowed these firms to have anticipated the potential risks they faced.[xxxiv] Proper identification, assessment and mitigation strategies will lead multinationals looking at a market like Nigeria, to take measures such as 1) purchasing political risk insurance, 2) negotiating more favorable production sharing agreements at the frontend, 3) including detailed descriptions, regarding the discovery and distribution of oil and gas in business-government agreements, 4) establishing and protecting supply chains, and monitoring legal and regulatory shifts for adverse changes.

COUNTRY RISK INDICATORS FOR FRONTIER MARKETS

In addition to leveraging the J Curve, sophisticated market participants must also dive deeper. Questions of geopolitics, economics, demography and governance must also be explored. These factors will be explored below in our case study. However, I believe it necessary to contribute a brief note on geopolitics.

Brief: Geopolitics

Geography and politics are inextricably linked, knowing this will save time, money and a great many headaches. Therefore, understanding the frontier market’s neighborhood is important. Who are its neighbors? And what kind of relationships to they maintain? Boardrooms across the world are abuzz with these questions. According to a 2016 survey by McKinsey& Company, a global management consultancy, business executives believed that “geostrategic” risks were on the rise and that it could hurt company profits.[xxxv] Concerns were most prevalent in the high-tech, financial services and telecommunications industries.[xxxvi] Executives in critical industries are worried and for good reason, from constant Russian threats to shut down the flow of oil to Eastern and Central European nations,[xxxvii] the growing trade war,[xxxviii] insecurity abounds, so knowing and understanding geopolitical trends in critical.

Having considered the systemic/international concerns, we must also remember that internal national factors are crucially important as well. Kazakhstan provides a perfect example of a frontier market. By analyzing the country’s governance structure, demography, economics and key risk factors, we can gauge the level of instability and ease of doing business in the country.

CASE STUDY: KAZAKHSTAN

Background

With a population of almost 18 million and a per capita income of US$8,710, Kazakhstan exhibits some of the features that would define it as a frontier market.[xxxix] Wedged between Russia and China on the Eurasian steppe, Kazakhstan is a mineral and energy rich nation on the path to strong economic growth.[xl] Following the collapse of the Soviet Union and independence in 1991, the country saw dynamic growth through their oil and gas sector. According to the World Bank, Kazakhstan’s economy grew by over 4% year-over-year in the first half of 2017 with oil and gas being the main economic drivers.[xli] So, at least from a macro-perspective, the country appears to have potential.

Governance and the J Curve

After decades of vassal-status under the Soviet Empire, Kazakhstan declared its independence in 1991 (as a result of the Soviet Union collapsed that same year). However, in true Soviet style, since independence, the country has been ruled by the same man, 78 year-old strongman, Nursultan Nazarbayev;[xlii] thus placing the country firmly on the upper-left of the J Curve. Corruption and a lack of accountability are deeply engrained in the country’s governance structures.[xliii] According to Transparency International’s 2017 Corruption Perception Index, Kazakhstan ranked 122nd out of 188 countries and only scored 31 out of 100 for corruption. [xliv] Although the government is hungry for economic growth, policy-wise they appear to be reluctant to implement policies to open up the economy and promote a high-skilled work force, leading to poor regional trade ties and oversized government involvement in the economy (state-owned entities dominate the marketplace).[xlv]

As such, international market participants will have to seek ways to work closely with the government and create joint ventures with governmental stakeholders to get involved. On an encouraging note, the government has been taking steps to work with the European Union and the United States to strengthen its judicial system to combat endemic corruption.[xlvi] Although important reforms have been made in recent years to curtail money laundering and corruption, and strengthen competition, the corporate legal framework still falls far behind international standards.[xlvii]

All of these government factors may be interesting but the question remains, what does it mean for business? Well, according to Santander, a global financial institution, Kazakhstan was able to attract over US$20Bn in foreign direct investment inflows, primarily in the oil and gas sector;[xlviii] so international market participants are taking notice. The country is by no means perfect in its reformation and there remain key factors that can be either positive or negative, depending on how much risk a company eager to invest in Kazakhstan is willing to take on. Still, with a poor human rights record and concentration of power in the presidency, multinationals will have to consider the extent to which these risks can influence their decision to engage with what is arguably a frontier market ripe for exploration.

Two key factors, amongst many, that are also important to look at for this frontier market are demographics and economics. These factors have contributed to both its risk factors and attractiveness.

Demography

As Kazakhstan continues down the road, at least to some degree, of reformation and liberalization, the population structure can and will play a major role in shaping the country’s next few years. Forecasting risk in the social and political realm therefore relies on Kazakhstan’s population age structure. Countries with large percentages of younger adults, old enough to be part of the labor force, have traditionally had less of a chance of attaining and maintaining open democratic governance than countries with older age structures.[xlix]

The above population pyramid[l] appears to demonstrate a youth bulge between the ages of 20 and 35; however, it also demonstrates a decrease in the youth population that immediately follows.[li] With a smaller youth bulge, there will be less jostling and less competition for inclusion in the labor market, and access to a limited pool of jobs, educational and health resources. This has positive societal implications and will help into creating an environment more capable of fostering economic growth and raising the economic prospects for more citizens.[lii]

These demographic trends can portend a potential environment of stability; key for multinationals wishing to take advantage of potential opportunities in this frontier market. However, as the earlier discussion regarding the J Curve has displayed, transitioning from a closed stable country to an open stable country is complex, dangerous and wrought with uncertainty. As such, another element of demographic risk is also a cause for concern. However, given the last elections in the country were Nazarbayev received 98% of the vote, barring unforeseen factors; this will remain a closed autocracy.[liii]

Economics

Kazakhstan continues to try to, slowly, recreate its economic system to attract more private investment and develop a free market business environment.[liv] However, serious issues remain, corruption remains a huge problem in the economy dragging down reforms and stymying genuine growth and economic potential. Further, the legal system remains opaque and unfriendly to international market participants.[lv] Beyond the corruption and graft, the country’s economic growth is largely tied to commodities, particularly oil. With the recent fluctuations in oil and gas prices, this makes for a relatively unstable environment.[lvi] However, other areas of the economy have seen growth including agriculture, manufacturing, transport trade sectors, and transportation.[lvii] The country continues to implement reforms to privatize many of the state-owned entities. Both factors may portend an opportunity for market participants to invest and enter into a broader marketplace, without necessarily engaging in the oil and gas sector.[lviii]

Furthermore, Nursultan Nazarbayev’s January 31, 2017 statement in which he pledged to join the World Economic Forum’s 30 developed and competitive economies, demonstrates a potential commitment to greater liberalizations and a commitment to the necessary political and policy reforms.[lix] To that end, the country has made some progress climbing from 72nd in 2011 to 53rd in 2016 out of 138 countries ranked by the World Economic Forum.[lx] As the economic system develops, some of the cross-sectional key risk factors must be reviewed to determine the true political risk in investing in Kazakhstan.

Key Risk Factors

| Kazakhstan[lxi] | Government Stability | Military in Politics | Religious / Ethnic Tensions | Corruption | Ease of Doing Business |

| Grade | B- | B- | D | C | B |

| Reasoning | Given the sham elections in 2015 and Nursultan Nazarbayev stranglehold on power, and his alliance with the United States, it appears that Kazakhstan will remain a closed but stable nation for the time being.[lxii] | The country’s fate and power appear to lie solely with its autocrat. Although, the military don’t appear to play the same role as say Myanmar (by comparison). Autocracy remains a major issue.[lxiii] | Inter-ethnic clashes between the Tajik and Kazakh populations remains persistent in the country. The government is reluctant to deal with the reality of the issue and allows it to fester beneath the surface.[lxiv] | According to Transparency International’s 2017 Corruption Perception Index, Kazakhstan ranked 122nd out of 188 countries and only scored 31 out of 100 for corruption.[lxv] Corruption remains a persistent problem in the country. | The World Bank Group has increased the business ranking slightly for Kazakhstan. Protecting minority investors and registering property in the country has become easier throughout the country.[lxvi] |

These risk factors demonstrate that there are upward trends in the country that can be a positive sign for both economic growth and stability. However, what remains clear is that the country still has many hurdles to overcome. As the government continues to liberalize the economy, instability may become a greater factor and inter-ethnic violence may become a major problem. Additionally, as the political system continues along the curve, companies must continually monitor for progress and backsliding towards a command economy. The country’s long term promise remains high and investors appear to be engaged. Investing in Kazakhstan as a multinational corporation will require robust ethics and conduct procedures that must be enforceable enterprise-wide.

Political risk insurance against regulatory change and creeping expropriation may also be a necessary element of any strong risk mitigation strategy; particularly for companies operating in Kazakhstan’s largest industry, Oil and Gas. A business continuity plan will also be a necessary part of any robust plan given the current violence and ethnic tensions flaring back up in the country. Investing in Kazakhstan remains a mixed proposition and clearly demonstrates the central need for political risk planning and management.

CONCLUSIONS

What we see here is that a robust strategy for frontier market entry relies heavily on the formulation of knowledge into a viable strategy, only then can market participants, over time, reap significant dividends. The risks that these companies face in frontier markets can be mitigated and managed if these companies can forecast potential problems through war gaming and identifying key risk factors.

A brief look at Nigeria gave an example of the potential for political risks while an in-depth study of Kazakhstan uncovered interesting governance, demographic and economic trends that shed light on the country’s predisposition towards instability, corruption, on one hand and economic promise on the other. What has been made clear is that investing in frontier markets amplifies the risk that multinational firms will face, and that developing strong and durable risk mitigation strategies matter. Frontier markets must be approached with caution and a strong interest in identifying, assessing and mitigating political risk.

[i] BRICS is an acronym for Brazil, Russia, India, China and South Africa.

[ii] Mangi, F. (2018, February 20). Look Out Emerging Markets, Frontier Stocks Are Set to Shine. Retrieved from https://www.bloomberg.com/news/articles/2018-02-20/value-seekers-waking-up-to-frontier-stocks-tundra-fonder-says

[iii] Badawy, M. (2013, May 19). Analysis: Frontier Markets booming but risks mounting. Retrieved from https://www.reuters.com/article/us-markets-frontierfunds-risks-analysis/analysis-frontier-markets-booming-but-risks-mounting-idUSBRE94I06P20130519

[iv] Fitch: Frontier Markets Growth Slowed in 2016 but Trade Now Picking Up. (2017, July 03). Retrieved from https://www.reuters.com/article/fitch-frontier-markets-growth-slowed-in-idUSFit5X0BMD

[v] http://www.schroders.com/staticfiles/schroders/sites/americas/us%20institutional%202011/pdfs/talking-point-frontier-markets.pdf

[vi] MSCI Frontier Market Index (2018, May 31). https://www.msci.com/documents/10199/f9354b32-04ac-4c7e-b76e-460848afe026

[vii] TIAA-CREFF, “Frontier Markets: An opportunity for growth and diversification” (May, 2015) https://www.tiaa-cref.org/public/pdf/C23893_Frontier_Markets.pdf

[viii] Ibid.

[ix] Finance and Economics Section, “Wedge Beyond the Edge: Money is leaving emerging markets for riskier bets at the investment frontier” The Economist, (April 5, 2014) http://www.economist.com/news/finance-and-economics/21600132-money-leaving-emerging-markets-riskier-bets-investment-frontier-wedge

[x] “How managing political risk improves global business performance,” PwC Advisory and Eurasia Group, 2010

[xi] Ibid.

[xii] What is political risk? (2017, June 08). Retrieved from https://www.economist.com/the-economist-explains/2017/06/08/what-is-political-risk

[xiii] “Managing Political Risk: Controlling Loss, Finding Opportunity”, Accenture, (May 2012) pp.1-12

[xiv] Michael H. Moffett, et al., “Fundamentals of Multinational Finance”, Pearson (2013) Ch.17

[xv] Ibid.

[xvi] “Managing Political Risk: Controlling Loss, Finding Opportunity”, Accenture, (May 2012) pp.1-12

[xvii] Ben Sheppard and Mary Crannell, “The decision gym: decision insurance for organizations” The Environmentalist, Volume 32, Issue 4 (December 2012)

[xviii] Ibid.

[xix] “Managing Political Risk: Controlling Loss, Finding Opportunity”, Accenture, (May 2012) pp.1-12

[xx] Ibid.

[xxi] “Integrating Political Risk Into Enterprise Risk Management” PwC and Eurasia Group, (2015) p.28

[xxii] This is based on an analytical framework developed by Ian Bremmer in his book “The J Curve: A New Way to Understand Why Nations Rise and Fall”

[xxiii] Ian Bremmer, “The J Curve: A New Way to Understand Why Nations Rise and Fall”, The Economist (2006) Ch.1 p.6

[xxiv] https://www.economist.com/books-and-arts/2006/08/31/the-geometry-of-geopolitics

[xxv] Ian Bremmer, “The J Curve: A New Way to Understand Why Nations Rise and Fall”, The Economist (2006) Ch.1 p.6

[xxvi] Ibid.

[xxvii] PwC, “How the J Curve can help companies to understand and manage political risk” (2012)

[xxviii] Ibid.

[xxix] Gavin Serkin, “Frontier: Exploring the Top Ten Emerging Markets of Tomorrow”, Bloomberg Financial, (2015)

[xxx] Lapegna, A. (2017, Dec 15) A Background on Nigeria and its oil Retrieved from: http://www.aspeninstitute.it/aspenia-online/en/article/background-nigeria-and-its-oil

[xxxi] Christopher Adams and Maggie Fick, “Western oil groups warn against Nigerian Contracts overhaul”, (October 11, 2015) http://www.ft.com/intl/cms/s/0/6e6fa2de-6e8c-11e5-8171-ba1968cf791a.html#axzz3tppDMxTG Accessed: December 9, 2015

[xxxii] Ibid

[xxxiii] Arch Puddington, “The Troubled State of Freedom in Nigeria” Freedom House, (April 16, 2014) https://freedomhouse.org/blog/troubled-state-freedom-nigeria Accessed: December 9, 2015

[xxxiv] Christopher Adams and Maggie Fick, “Western oil groups warn against Nigerian Contracts overhaul”, (October 11, 2015) http://www.ft.com/intl/cms/s/0/6e6fa2de-6e8c-11e5-8171-ba1968cf791a.html#axzz3tppDMxTG Accessed: December 9, 2015

[xxxv] Geostrategic risks on the rise. (n.d.). Retrieved from https://www.mckinsey.com/business-functions/strategy-and-corporate-finance/our-insights/geostrategic-risks-on-the-rise

[xxxvi] Ibid.

[xxxvii] Ukraine closes airspace to all Russian planes. (2015, November 25). Retrieved from https://www.bbc.com/news/world-europe-34920207

[xxxviii] https://www.cnbc.com/2018/03/21/white-house-to-announce-ip-tariffs-on-thursday-sources.html

[xxxix] World Bank Group, “Ease of Doing Business in Kazakhstan,” Doing Business 2018, http://www.doingbusiness.org/data/exploreeconomies/kazakhstan

[xl] https://www.bbc.com/news/world-asia-pacific-15263826

[xli] http://www.worldbank.org/en/country/kazakhstan/publication/economic-update-fall-2017

[xlii] https://www.britannica.com/biography/Nursultan-Nazarbayev

[xliii] https://www.usaid.gov/kazakhstan/democracy-human-rights-and-governance

[xliv] https://www.transparency.org/country/KAZ#

[xlv] http://www.worldbank.org/en/country/kazakhstan/publication/economic-update-fall-2017

[xlvi] https://eeas.europa.eu/headquarters/headquarters-homepage/36413/eu-and-kazakhstan-hold-subcommittee-justice-and-home-affairs-and-human-rights-dialogue_en;

[xlvii] https://www.ebrd.com/legal-reform/where-we-work/kazakhstan.html

[xlviii] https://en.portal.santandertrade.com/establish-overseas/kazakhstan/investing

[xlix] Richard P. Cincotta, “Half a Chance: Youth Bulges and Transitions to Liberal Democracy”, Wilson Center, ECSP Report, Issue 13, 2008 – 2009, p.11

[l] https://www.cia.gov/library/publications/the-world-factbook/geos/kz.html

[li] Ibid.

[lii] Richard P. Cincotta, “Half a Chance: Youth Bulges and Transitions to Liberal Democracy”, Wilson Center, ECSP Report, Issue 13, 2008 – 2009, p.11

[liii] https://www.cnbc.com/2018/01/16/kazakhstan-is-a-kleptocracy-ruled-by-an-autocrat-its-also-an-increasingly-important-strategic-ally.html

[liv] http://apps.export.gov/article?id=Kazakhstan-Market-Challenges

[lv] Ibid.

[lvi] Ibid.

[lvii] http://www.worldbank.org/en/country/kazakhstan/publication/economic-update-fall-2017

[lviii] Ibid.

[lix] https://primeminister.kz/en/news/all/the-president-of-kazakhstan-nursultan-nazarbayevs-address-to-the-nation-of-kazakhstan-january-31-2017-14017

[lx] http://apps.export.gov/article?id=Kazakhstan-Market-Overview

[lxi] The grading in this table is from the author.

[lxii] https://www.cnbc.com/2018/01/16/kazakhstan-is-a-kleptocracy-ruled-by-an-autocrat-its-also-an-increasingly-important-strategic-ally.html

[lxiii] Ibid.

[lxiv] https://eurasianet.org/node/72006

[lxv] https://www.transparency.org/country/KAZ#

[lxvi] http://www.doingbusiness.org/data/exploreeconomies/kazakhstan